Klarna Financing is great for borrowing money, especially if you want to buy something from its partner US retail stores that accept debit or credit cards as payment options. Like its popular competitors, Klarna will allow you to borrow money using its app and pay the sum over time. In the process, Klarna reviews your and any other buyer’s financial and credit backgrounds to ensure it maintains a standard. However, is Klarna safe to use? What are some drawbacks if any? Will you need to pay high-interest rates?

This article reviews Klarna Financing and its services. We will give you the pros and cons to help you understand it and determine whether it’s good or not for your budget.

Also read: Top 15 Budget Apps You Need to Use

Inside This Article

How Klarna Financing Works

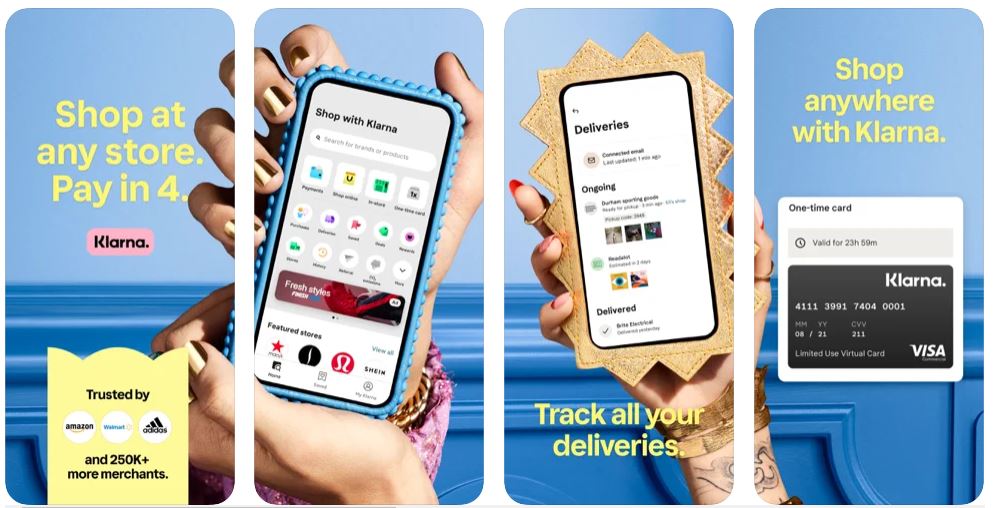

First things first. What is Klarna and how does it work, you ask? In essence, Klarna is an alternative to credit cards or traditional loans services. To elaborate, it helps you split the bill for a purchased item and lets you pay the remaining balance through installment.

When it comes to your expectations about it, though, you must be realistic — there are fees and interest charges to pay indeed. Many people are drawn to Klarna because of its zero annual fee charge feature and absence of membership fees. However, Klarna charges fees and interest rates depending on the payment type you choose.

PROS

- 1. No annual and membership fees are required

- 2. Offers flexibility to consumers on purchase options

- 3. Can be used at any US retail store easily

CONS

- 1. Only offers a small loan amount

- 2. Charges fees for late repayments

Though paying upfront through cash is preferable, using Klarna as a payment method for items that are out of your paygrade at the point of purchase makes sense. That is as long as you are comfortable with the fees and interest rates that may come with your payment method of choice.

Furthermore, Klarna requires a minimum purchase of $10 but it does not specify a maximum purchase limit — as long as you can use your credit card or chosen payment method for the remaining balance. To give a specific context or example of how Klarna works, take an item that’s worth $200. At the checkout counter, you only have to pay $50 cash upfront when using Klarna. The remaining $150 will be split into three payment cycles. Scroll down this article to find out what Klarna’s other payment methods are.

Klarna Review: Things You Need to Know

Let’s now take a closer look at Klarna’s terms and conditions and try to answer the question, “Is Klarna safe to use?” The succeeding sections will broaden your knowledge about the financing app and service. In the end, we want to help you decide whether Klarna is the right match or not for your purchasing habits.

Repayment Options

Many consumers use Klarna at buy-now-pay-later stores, including Sephora and Etsy. That is because the app offers flexibility in terms of purchase options. But how can you repay Klarna? What are Klarna’s repayment options? Below is a table outlining Klarna’s repayment option schemes. See whether any of these works for you.

| Terms & Conditions | Amount to Pay at Checkout | Interest Rates | Late Repayment Fee | |

| Four Installments | Pay a quarter of the total amount due (first installment). The remaining balance will be billed to the buyer’s registered credit card every two weeks following the first payment. | A quarter of the amount due (first installment) | No interest rate applies | Up to $7 |

| Pay in 30 Days | Pay no amount upon checking out. The 30-day payment period will start after the item has been shipped. | $0.00 | No interest rate applies | Late repayment does not apply if the customer pays the due amount on time. |

| Credit Card | Pay the full amount using a credit card or debit card through the Klarna app. | Full amount | No interest | No late repayment fee applies. |

| Financing Account | Fund a purchase for six to 36 months. | $0.00 | A figure that might be higher than your credit card’s APR | Up to $35 |

Although Klarna does not charge you an annual fee, it is important to understand that late repayments incur charges depending on the payment method chosen. These late repayment fees range from $7 to $35, which is more or less equivalent to an annual fee charged by traditional credit cards or loan services.

Hence, before you make a purchase and use Klarna, check your budget and look at the bigger picture. Klarna’s terms and conditions are enticing and seem safe but a second look at your personal finances will not be bad, too.

Warranty or Return Protection

Klarna reviews its operations regularly and that includes doing credit checks on you before approving your application. Part of being approved to use Klarna’s services is a buyer’s protection policy. The policy was designed to ensure customers don’t have to pay anything in the likely event something goes wrong with the purchased item. Let’s have a closer look at that policy; what it covers and how it can protect buyers like you.

Buyer Protection Policy

Below are provisions under Klarna’s Buyer Protection Policy:

- In case of failure to receive items bought: Klarna will not ask you to pay for anything if the item has not been shipped yet or did not arrive, which is typical in similar apps or services. That is only if you have picked the Pay-in-30-Days method. In case of delays, you can contact Klarna’s customer service to double-check where the items are at or whether mitigating circumstances are delaying the shipment of the item or not.

- In case the item has already been paid for: In case you did not receive the paid items on the due date, you are advised to check the invoice for missed information. This applies to anyone who opted to pay using the Pay Later (30 Days) method, a credit card, or bank transfer. You can then coordinate with the store’s customer service for shipment details. Lastly, you can contact Klarna’s customer service and ask that the matter be investigated further. What is good about this is that both Klarna and the partner store can be alerted about the problem.

- Refund Policy: You are entitled to a refund under certain conditions. Essentially, you have to inform both Klarna and the store where the item was bought if you wish to use your cancellation rights. However, failure to inform Klarna and the store might result in (1) ineligibility for a refund and (2) you, the buyer, paying for the amount due even if the item has not been received yet. Moreover, Klarna may either request for payment or withhold succeeding payments if the item has been held by Customs. This kind of refund policy that keeps all parties in check seems just right.

Return and Cancellation Policy

Below are provisions covering the Return and Cancellation Policy by Klarna:

- In case of damaged and wrong items delivered: Before shipping, Klarna reviews all items as part of the quality assurance process. But there are still cases wherein buyers report they got a defective or wrong item. In cases like those, you will not pay for the item you report as defective. Again, this is provided that you have opted for the 30 Days Pay Later method. You are also advised to (1) contact Klarna’s customer service to suspend any payment due and (2) contact the merchant for possible resolution.

- In case you want to cancel an item: Klarna will refund you for the total cost and delivery if you have the right to use your cancellation right as afforded under the Consumer Contracts Regulations 2013. Additionally, Klarna may opt to deduct shipping costs if you want to cancel a purchase with respect to the merchant’s policy.

As a buyer, you maintain your right to cancel a purchase from the buying date up to 14 days upon receiving the item. You are given 14 days to return the item.

Promotional Offers and Rewards

Like any other financial service, Klarna reviews your purchase patterns and behaviors and offers rewards for every one of them. That makes the deals even “sweeter” — you get to pay for things in increments and gain gift cards and more in the process. Also, since Klarna is a partner of many known US retail stores, you can earn reward points called Vibe Perks that you can use in the form of discounts.

Below are some of Klarna’s partner merchants where buyers can earn Vibe Perks.

How do you take advantage of special promotions and rewards through Klarna, then? Here’s how:

- Download the Klarna app and sign up for Vibe.

- Once signed up, start using Klarna as your payment method to earn $1 Vibe.

- Collect Vibe points and use them as rewards on your next purchase.

Learn More About Klarna Rewards

Klarna Customer Service

Klarna offers a wide range of customer solution categories — from general inquiries and payments to fraud and security. You have three ways to reach Klarna’s customer service:

- There is a customer service option in the Klarna app. You can track deliveries, manage payment issues, and settle possible refund or cancellation requests. Additionally, you can also get 24/7 chat support from the Klarna app.

- You can try to find a resolution to any Klarna-related issue by visiting the Customer Service Page. The page covers several resolution categories that buyers like you will surely find helpful one way or another.

- Lastly, you can chat or call any Klarna customer service representative via Klarna Chat Support. Alternatively, you may call 844-KLARNA1 (844-552-7621).

Bonus FAQs About Klarna

At this point, you already know that Klarna reviews your credit history, conducts quality assurances, has flexible repayment methods, and offers resolution to buyers’ issues. Is Klarna safe, then? Based on everything we’ve discussed so far, it is safe. So, let’s now deal with other possible questions you have in mind, which other customers also ask. How does Klarna make revenue to fund the loans it offers? Moreover, does it help you build credit? Below are our answers.

1. How Does Klarna Earn Money?

Klarna’s business model is not far off from the models employed by the likes of Afterpay, Affirm, or other apps like Dave. Essentially, Klarna charges e-commerce merchants a fee as part of the bilateral service agreements. That covers set-up and monthly fees, and a fraction of the fee for every transaction made. The exact details on how the company charges stores and the range would naturally depend on what is agreed upon by the said two parties. However, it has been reported that Klarna charges $600 for setup fees and a $90 monthly fee, and gets 1.5 to 3% for each transaction.

Moreover, Klarna also earns by charging customers who pay late and those who are acting as payment processors. This is not a question considering Klarna has operations in 17 countries and caters to up to 90 million shoppers.

2. Does Klarna Build Credit?

Klarna reviews financial standing through a battery background check. It is straightforward in informing its potential and existing customers about that. If you are using Klarna, you may find that your credit scores are not affected when opting for the following:

- Payment using the Pay-in-4 Installments method

- Payment using the 30 Days Pay Later method

Your credit score might only change in relation to using Klarna when the following are met:

- You apply for one of the Klarna Financing options

- You take out a standard payment holiday for Klarna Financing options

Klarna further expresses that when you opt for Klarna Financing, a credit check would be conducted. That will then be visible to other lenders as part of their credit report, thereby affecting credit scores.

Klarna Review: The Verdict

Our verdict is clear: Klarna is a decent lending service option and can be as good as any other alternative out there. Below are our detailed explanations on what can make you switch to it or not. All in all, we think the pros outweigh the cons.

What We Like About Klarna

Looking at user reviews alone, we can affirm the ease at which buyers can sign up for an account using the Klarna app. Moreover, we appreciate the absence of charging annual and membership fees from customers. The idea that late repayers will incur fees is nothing new; the same is true with other traditional credit card and loan services.

On top of that, we love how Klarna offers flexible repayment methods that will surely fall within a buyer’s capabilities to repay. Klarna is also upfront on matters concerning its resolve to help its customers become responsible lenders, its buyer protection policies and coverages, and how its services may or may not affect someone’s credit scores.

The bottom line: We suggest Klarna for borrowers who want to purchase a big-ticket item and have the means to pay for that without necessarily going broke over time.

What We Don’t Like About Klarna

Nothing is glaring in the terms and conditions that would make us think otherwise of Klarna. It is a decent lending service alternative and can compete with other services of its kind. Perhaps, Klarna’s lack of a purchase ceiling limit is the only thing that is concerning. That is because it may encourage buyers to borrow more than what they could afford. However, on the side of the borrower, it must be factored in that Klarna only offers a small loan that could affect one’s purchase flexibility.

If you are looking for an alternative buy now pay later app, here are a few apps like Klarna that you can try.