Buy now, pay later apps are incredibly useful, especially if you find yourself out of cash for the month. They’re great for urgent purchases, which you can pay in smaller installments later on. Best of all, unlike credit cards, buy now, pay later apps usually ask for no interest. Which buy now, pay later apps are worth trying in 2021? Here are our top 13 picks just for you.

What Are Buy Now, Pay Later Apps?

In the modern day, we have numerous apps that can do almost anything for us — including managing our finances. Money transfer apps or cash advance apps like Dave supplement our finances and alleviate a few burdens. Likewise, buy now, pay later apps play a role for folks struggling with cash flow.

Buy now, pay later apps do exactly what they imply. They’re apps that you can use to purchase items this instant without having to pay upfront, like a credit card. You can pay them in installments over a set period (usually in four separate payments) later on.

What makes them enticing is that they usually don’t charge interest, unlike credit cards. Their approval systems are also less strict, so you can apply for them more easily. Of course, making late or failed payments still result in penalties, so you’ll still have to be careful.

Buy now, pay later apps are different from loan and cash advance apps. Typically, the latter requires you to deposit earned income into a checking account before your paycheck arrives. As the name implies, they’re apps that give you cash in advance before your next payday. On the other hand, buy now, pay later apps allow you to shell out money you don’t have. You’ll have to take charge of the financing and payments later on, without the app tinkering with your paycheck whatsoever.

Cash advance apps are handy for emergencies, especially if buy now, pay later apps aren’t partnered with your chosen retailer. However, each one has its unique pros and cons and will be handy in different circumstances.

Best Buy Now, Pay Later Apps

What are the best buy now, pay later apps you can use in 2021? Here are our top picks in alphabetical order.

1. Affirm

One of the most convenient buy now, pay later apps is undoubtedly Affirm. The reason for this is simple: Affirm, unlike many credit-based apps, charges no fees even if you pay off your loan late on the due date. Hence, you won’t have to worry about paying more than the amount you borrowed if you’re ever late on a payment.

When it comes to interests, Affirm is great because its charges on certain transactions are simple. Hence, you don’t need to worry about exponential growth in interest. Of course, the downside to this is that Affirm does charge interest, unlike other buy now, pay later apps. These can range from 0% to 10% or even 30%, depending on the store. As a result, it’s not exactly ideal if you wanted an app that charges no interest at all.

Nonetheless, Affirm is great if you like flexible, long-term payment plans. That’s because the app allows you to pay in three to 36 months (again, without any fees). Moreover, it’s one of the most excellent buy now, pay later apps if you need to make large purchases because of its $17,500 transaction cap.

Affirm is widespread, which means you can shop from many online and physical stores with it. If a store isn’t partnered with Affirm, you can generate a virtual card number instead. Best of all, the app doesn’t have a minimum credit history so you’ll have no trouble getting approved.

Adore

- No late fees

- Flexible payment scheduling

- Large maximum limit

- Online or physical purchases available

DISLIKE

- Interest in some transactions

- Needs a credit check

- No physical card

Download Affirm on Google Play Store

2. Afterpay

We couldn’t leave out Afterpay when it comes to the best buy now, pay later apps. For those who want a loan but remain on a budget, this app has a handy smart credit limit feature that keeps you from going overboard with your credit-based purchases.

In addition, Afterpay is also mindful about helping you make your payment deadlines by sending reminders of your payment schedule. However, it is a little punishing if you’re late on the payments. That’s because, while there are no fees for on-time payments, late payment fees can be very high.

Moreover, Afterpay is a bit picky when it comes to the orders you make. The app has to approve each purchase you make and can even decline one if it deems necessary. It is still good if you need an external force to keep your spending under control, regardless.

Afterpay lets you divide your payments into four no-interest installments if your purchase is not over $100. It has over 85,000 partner brands, so you’ll have tons of retailers to choose from. You can also shop offline via Afterpay’s virtual card number, so you’re not limited to online shopping.

Adore

- Helps you budget through smart credit limits

- Sends payment reminders

- No fees for on-time payments

DISLIKE

- The app can decline your purchase

- High late fees (up to 25% of the order amount)

- Approval per purchase

Download Afterpay on Google Play Store

Download Afterpay on App Store

3. Fingerhut

Fingerhut is one of the best buy, now pay later apps for those who need credit without a good score. It doesn’t review your credit history at all to get you approved to start with. Thus, even those with a bad credit history can apply and get approval. The good thing, though, is Fingerhut is a good place to start boosting your credit scores. Good payment behavior on the app reflects on your account with all three major credit bureaus. It also provides no annual fees whatsoever that could further burden your payment.

However, Fingerhut does have tons of disadvantages that you’ll have to bear with just to boost your credit score. For one, they only allow you to purchase from their website or partner retailers. Moreover, the prices on their website are sky-high, with a 29.99% Annual Percentage Rate. There’s also a $38 fee for returned or late payments.

With that in mind, Fingerhut isn’t the best of the buy now, pay later apps on this list. Nonetheless, it’s decent if you’ve been denied everywhere else and want credit regardless of your score.

Adore

- No reviews for credit history

- Zero annual fee

- Good payment behavior helps your credit score

- Split payments in 6 or 8 installments

dISLIKE

- Higher prices

- Only allows you to purchase from Fingerhut or its partners

- Large interest rates and fees

Download Fingerhut on Google Play Store

Download Fingerhut on App Store

4. Four

Number four on our list is Four. It’s not exactly the most popular service out there, but it’s certainly worth considering given its benefits. That’s because Four not only splits your payments into 4 equal installments, but it also offers no fees or interests.

It is also great for users who are looking for burden-free buy now, pay later apps. None of your payment behavior within the service will reflect on your credit score. Hence, you don’t have to worry about late payments affecting your score whatsoever.

The only downside with Four is that it requires you to pay 25% upfront. Hence, you’ll still need to pay for the down payment and shell out some cash. Nonetheless, it’s a great option since you get to pay the balance over 6 weeks. All you’ll need to do is sign up, link your card (or Apple Pay or Google Pay) and you’re ready.

Adore

- No hidden fees

- Interest-free

- Split between four equal payments

- No reflection on credit score

dISLIKE

- 25% upfront payment

Download Four on Google Play Store

5. Klarna

A lot of buy now, pay later apps provide a good short-term solution for financing your purchases. However, it’s not always practical to finance larger purchases in short-term installments. That’s why Klarna is one of the best pay later apps if you’re buying more expensive items.

With Klarna, you can have up to three years of financing for your transactions. Hence, you can pay in smaller, more manageable installments over a longer period. That said, you can also choose shorter payment periods (as short as 30 days) if you desire.

Apart from this, Klarna is accepted nearly everywhere. Not only has it 250,000 partner retailers internationally, but it’s also accepted anywhere credit cards are. In addition, it’s also incredibly secure, providing dummy credit card numbers for each transaction to ensure security.

However, Klarna isn’t perfect. That’s because each transaction requires approval from the company (which is understandable given how they accept larger purchases). It also requires a credit check for certain financing options.

Adore

- Accepted wherever credit cards are

- One-time card numbers for security

- No interest or fees for on-time payments

- Rewards program

Dislike

- Approval per purchase

- Requires credit check

Download Klarna on Googe Play Store

Also read: Apps Like Klarna for Splitting Payments

6. PayPal Credit

One of the most prominent buy now, pay later apps is none other than PayPal Credit. As the name implies, the service is accepted anywhere PayPal payments are. Hence, you can use it almost anywhere internationally.

PayPal Credit offers flexible financing that doesn’t have monthly installment deadlines. That’s because the service simply asks you to pay the full balance within six months after the transaction. You don’t need to worry about shelling out some money every two weeks or so. PayPal Credit also comes instantly, which is great since other cards take over a week to arrive.

Unfortunately, it’s a bit complicated to get PayPal Credit. For example, the minimum line of credit is $250. You can only have 0% interest on your transaction if it goes over $99. In addition, the way its system works makes it so that bad performance only hurts your credit score. Hence, good payment behavior isn’t rewarded, but bad payment behavior is punished.

Adore

- Arrives instantly

- No set installment presets, just a deadline

- Accepted anywhere PayPal is

Dislike

- Reflects only negative behavior to credit bureaus

- Minimum purchase required for 0% interest

Download Paypal on Google Play Store

7. PayPal Pay in 4

If you need a small credit-based solution, then PayPal’s “Pay in 4” service is one of the best choices. Not only it provides the security of PayPal, but it also provides interest-free purchases. Hence, you won’t need to worry about the app’s reliability or paying a higher amount just for financing.

One of the best parts about it is that it’s accepted by millions of online stores, and you don’t need to consider compatibility most of the time. The only problem is that it isn’t available in every US state, so you’ll have to check for availability first.

Unfortunately, PayPal Pay in 4 can’t handle larger transactions. Unlike other buy now, pay later apps, Pay in 4 has a $600 maximum limit (and a $30 minimum). Hence, you’ll have to turn to other options if you want to make a larger purchase. The app also requires approval per purchase, so you can’t spend as freely.

Nonetheless, it’s a good choice if all you want to finance are small transactions. With Pay in 4, all you’ll need to pay upfront is a down payment. Afterward, you can pay in three installments in 15-day intervals. You can access this payment method on the Paypal app alongside PayPal Credit.

Adore

- Trusted brand

- Interest-free

- Accepted by millions of online retailers

Dislike

- $600 limit per purchase

- Not available in every North American state

- Approval per purchase

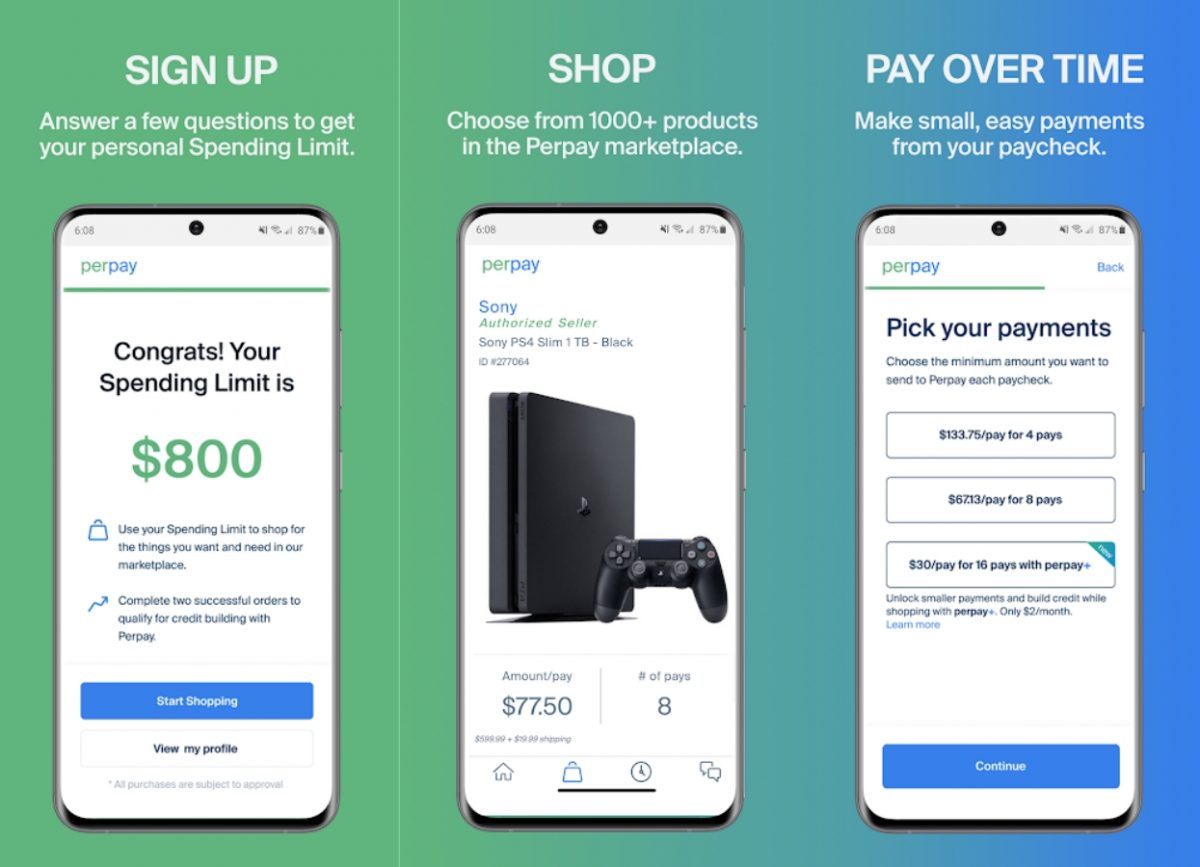

8. Perpay

The world isn’t exactly kind to people with poor credit histories. However, there are a few buy now, pay later apps that ease the burden and make financing easier. One of them is Perpay. How is it kind to those with bad credit? Simple: the app doesn’t screen users based on credit history, so it’s pretty accepting of everyone regardless of financial history.

Perpay isn’t exactly reckless with its services, either. It does enact some checks and balances to make sure it doesn’t lose money. One of the ways it does this is by limiting a user’s spending budget based on their income level.

Apart from this, Perpay acts like most other buy now, pay later apps. It provides a pretty lengthy financing period of up to six months — long enough to pay for most transactions. If you can pay on time, you can even raise your credit score through the app.

However, what the app does lack is the number of partner merchants it has. That’s because it only allows you to purchase from the company’s proprietary marketplace. Moreover, the items won’t be dispatched until your first payment. If that wasn’t enough, the app also requires you to pay through payroll direct deposit.

Nonetheless, the app is certainly worth considering since other buy now, pay later apps usually check your credit score. If you desperately need to improve your standing, it’s a decent way to do so.

Adore

- No credit history check

- Income-based limit

- 6-month financing period

- Boosts credit score for on-time payments

Dislike

- Limited marketplace

- Shipping only after the first payment

- Scheduled payments through payroll direct deposit only

Download Perpay on Google Play Store

9. Sezzle

If you have a bad habit of not making payments, then perhaps Sezzle would be a good choice. That’s because the app not only finances your payments over six weeks, but it also allows for payment rescheduling. Hence, you can push your payment back up to two weeks if you can’t make it in time.

Of course, this comes with a few conditions. The first reschedule per order is free. However, subsequent rescheduled payments will cost you $5. That isn’t so bad considering how little it is compared to your installment. Nonetheless, this fee can add up if you’re a serial rescheduler.

On the other hand, you can choose to reschedule multiple payments at the same time. Hence, you can push back all the subsequent payments through your first free reschedule. Through this, you can avoid the $5 fee altogether so long as you reschedule only once.

Beyond the rescheduling, Sezzle acts like most other buy now, pay later apps. It asks for a 25% down payment upon purchase which can be burdensome if you’re out of cash. However, it doesn’t charge any interest on your purchases, so at least there are no additional costs. On the other hand, Sezzle doesn’t have many partner merchants compared to other buy now, pay later apps. Hence, you’ll have to limit yourself to its 34,000 merchants to reap its benefits.

Adore

- Flexible payment plans

- Payment rescheduling up to 2 weeks

- No interest for purchases

Dislike

- 25% down payment

- Fee for additional payment reschedules

- $5 fee for additional rescheduling

Download Sezzle on Google Play Store

10. Splitit

Splitit purchases using your Visa or Mastercard credit card and earns rewards for you. However, unlike a regular credit card, Splitit splits your payment into installments and charges zero fees or interests. That is unless, of course, you make late payments.

The app doesn’t check your credit or require you to apply or register for anything before you can use it. The only requirement is that you must have a credit card already. It also uses your credit card’s current limit as its own; hence, you don’t have to adjust to a smaller credit limit like other buy now, pay later apps.

The only downside with Splitit is that it isn’t compatible with all types of other credit cards, particularly with Amex and Discover. Moreover, good payment performance on Splitit won’t affect your credit score at all.

Adore

- No registration, application, or credit check

- Spending limit based on your credit card limit

- High transaction approval rate

- No interest or fees

Dislike

- Requires a credit card before you can access it

- Does not help your credit score

- Not available with certain cards like Discover or Amex

11. ViaBill

Another great credit-based app is ViaBill. Like most buy now, pay later apps, ViaBill allows you to pay in four equal installments, with the first one upfront. However, the remaining three will be split equally, paid monthly.

One of the best parts about ViaBill is that it charges no interest or hidden fees on any transaction. Moreover, there are no late fees either since your registered payment method will be automatically charged each deadline.

However, you will have to contend with the fact that you’ll get a $300 initial credit limit. That’s not a lot for large spenders, but it’s a decent choice if you want financing that isn’t as burdensome as other buy now, pay later apps.

Adore

- No credit checks required

- Interest-free

- Monthly installment payments instead of bi-monthly

Dislike

- 25% upfront payment

- Small initial limit ($300

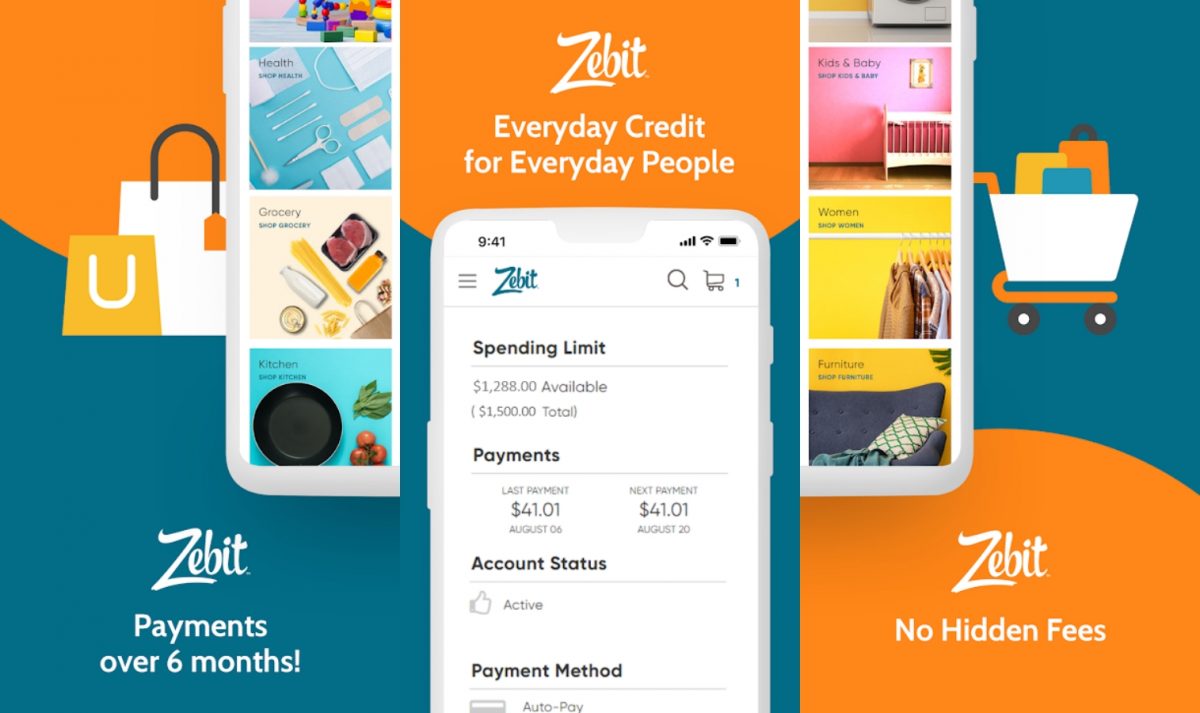

12. Zebit

Zebit is another buy now, pay later app that doesn’t put too much pressure on the user. That’s because it doesn’t require a good credit score and charges 0% interest. Hence, you can simply apply for the service and wait until you’re approved without worrying about your financial history.

In addition, the app also provides a pretty large limit and allows you to pay the balance across si months. You can have up to $2,500 worth of credit — enough for almost any kind of purchase you might make.

The downside to Zebit is that it only has 1,500+ partner brands. Moreover, you can only make purchases using Zebit from its proprietary online marketplace. Hence, it’s not the best choice if you want access to other retailers. Zebit also bases your ZebitLine on your current employer, so quitting your job will also cut your ZebitLine.

Adore

- 0% interest

- No credit score check

- $2,500 worth of interest-free credit

- 6-month financing

Dislike

- A small number of partner brands

- Only allows you to purchase from the Zebit Market

- Employer-based credit line

Download Zebit on Google Play Store

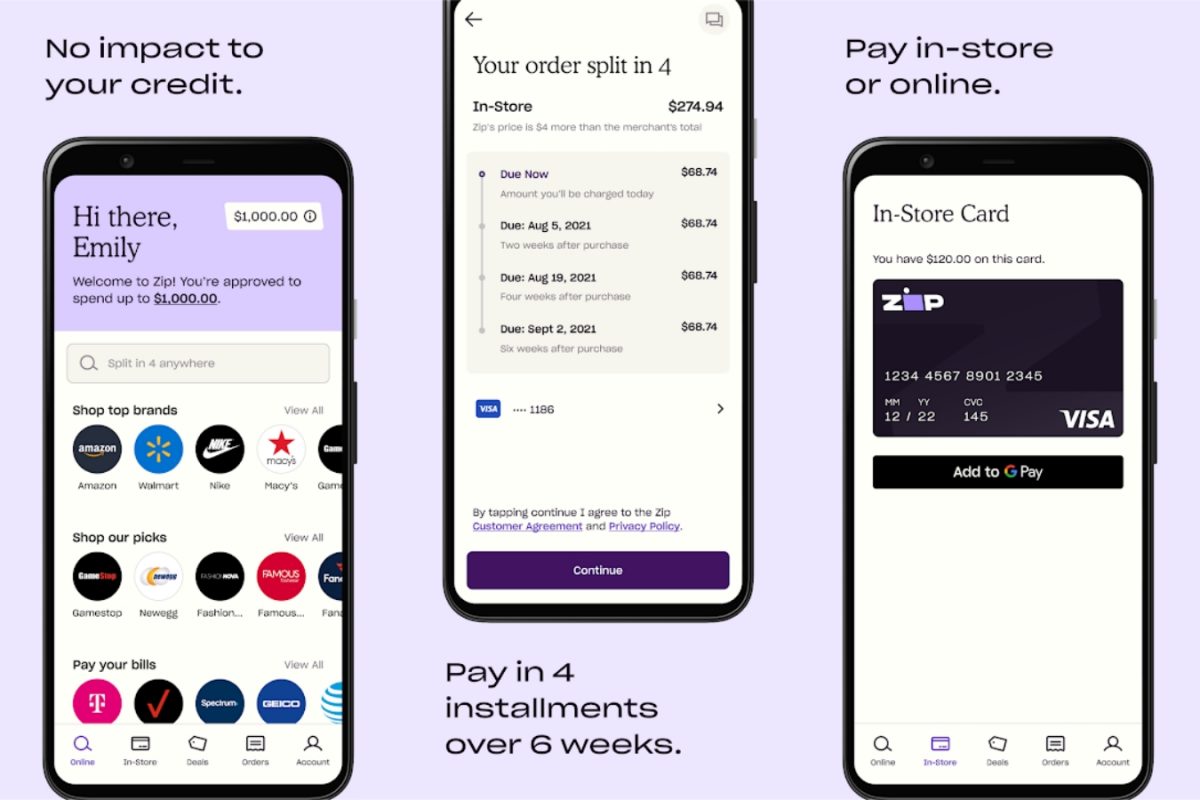

13. Zip (Quadpay)

Lastly, one of the best buy now, pay later apps is none other than Zip (formerly Quadpay). With Zip, you get easy access to proper financing without worrying about your credit history. That’s because the app doesn’t check your credit score before they approve your application. Moreover, Zip also doesn’t report your activity to any credit bureau in the US. Hence, you don’t have to worry about bad performance reflecting poorly on your credit score.

The only downside to Zip is how many fees it charges. For example, it has a $4 transaction fee per purchase (or a $1 fee per payment). The platform also charges a $7 late fee per late payment. With all of these combined, you can easily incur tons of expenses from the fees alone.

In addition, the app isn’t ideal if you’re looking for long-term financing. It only provides a six-week financing period and no more. The app might make up for it with its 51,000 international partner merchants and handy browser extension. However, it’s up to you whether the trade-offs are worth it or not.

Adore

- 0% interest

- No credit check

- Doesn’t report to credit bureaus

- 51,000 global merchants

- Browser extension available for non-partner retailers

Dislike

- 6-week payment period

- $4 fee per transaction or $1 fee per payment

- A fee of $7 per late payment

Download Zip on Google Play Store

The Bottom Line

If you’re living paycheck to paycheck, it’s easy to succumb to the allure of buy now, pay later apps. After all, sometimes you urgently need something but you don’t always have the money on hand. While we aren’t saying buy now, pay later apps are bad, we do urge you to spend your money wisely. These payment apps are convenient but can easily ruin your finances rather than help it if you’re not careful.